It’s satisfying to be your own boss—until you have to deal with health insurance. Finding reasonably priced health insurance as a freelancer might be difficult without an employer managing benefits. Your income may fluctuate from month to month, options are unclear, and premiums are expensive. The good news is that self-employed people do have access to reasonably priced health insurance. All you have to do is know where to seek and how to properly weigh your options.

In order to protect your health without breaking the bank, this article lays down every feasible route to affordable freelancer health coverage, including Medicaid, ACA Marketplace plans, HSAs, association plans, and more.

Why Health Insurance Is Non-Negotiable for Freelancers

Many independent contractors, particularly those who are just getting started, are tempted to forgo insurance in order to save money. That is a dangerous action. Tens of thousands of dollars can be spent on a single ER visit or unanticipated diagnosis, easily wiping out months’ worth of freelance income. Health insurance is more than simply a perk; it’s a financial safety net that prevents your freelancing career from collapsing when things become uncertain.

Beyond emergencies, coverage provides you with access to prescription medications, mental health services, and preventative care, all of which help you maintain optimal performance as an independent contractor.

How Much Does Health Insurance Cost for Freelancers?

Before exploring options, it helps to understand typical costs. On average, freelancers in the U.S. pay around $500 per month for individual health insurance. However, subsidies can dramatically change that number.

| Coverage Type | Estimated Monthly Cost | Best For |

|---|---|---|

| ACA Marketplace (with subsidy) | $0 – $200 | Low-to-moderate income freelancers |

| ACA Marketplace (no subsidy) | $300 – $600 | Higher-income freelancers |

| COBRA Continuation | $400 – $700+ | Transitioning from employer coverage |

| Spouse/Partner Plan | Varies (often lowest) | Married freelancers |

| Short-Term Health Plan | $100 – $300 | Temporary gap coverage |

| Association/Group Plan | $200 – $450 | Members of freelancer organizations |

Costs vary significantly by state, age, plan tier, and income.

Top Options for Affordable Freelancer Health Insurance

1. ACA Marketplace Plans (Healthcare.gov)

For most freelancers, the ACA Marketplace is the smartest starting point. These plans cover all essential health benefits — preventive care, emergency services, prescription drugs, and mental health treatment — and they cannot deny coverage based on pre-existing conditions.

The biggest advantage? Premium tax credits. If your projected annual income falls between 100% and 400% of the federal poverty level, you likely qualify for subsidies that lower your monthly premium considerably. In fact, nine out of ten people who enroll through the Marketplace receive some form of subsidy.

ACA Metal Tier Comparison:

| Tier | You Pay (Monthly Premium) | You Pay (When You Use Care) | Best For |

|---|---|---|---|

| Bronze | Lowest | Highest | Healthy, rarely need care |

| Silver | Moderate | Moderate | Most freelancers (unlocks Cost-Sharing Reductions) |

| Gold | Higher | Lower | Frequent healthcare users |

| Catastrophic | Very low | Very high | Under 30 or hardship exemptions |

Pro tip: If you qualify for Cost-Sharing Reductions (CSRs), you must enroll in a Silver plan to access them. This can dramatically reduce your deductible and out-of-pocket maximum.

Open enrollment typically runs from early November through mid-January. If you’ve recently left a job or had another qualifying life event, you may be eligible for a Special Enrollment Period (SEP) outside this window.

2. Medicaid (For Lower-Income Freelancers)

If your income falls below a certain threshold, you may qualify for Medicaid, which offers free or very low-cost coverage. Eligibility is based on your state and household income — generally at or below 138% of the federal poverty level in states that expanded Medicaid under the ACA.

Freelancers with variable income should check their eligibility each year, since a slow business season could make them newly eligible.

3. Spouse or Domestic Partner’s Employer Plan

If your spouse or partner has employer-sponsored health insurance, joining their plan is often the most cost-effective option available. Employer-subsidized premiums are typically much lower than individual marketplace rates, and you may pay significantly less out of pocket compared to any individual plan.

This option is worth seriously exploring before committing to a marketplace plan.

4. COBRA Continuation Coverage

Just left a full-time job? COBRA lets you continue your former employer’s group health plan for up to 18 months (and up to 36 months in some states and circumstances). It’s convenient because there’s no enrollment paperwork complexity and your coverage doesn’t change overnight.

The catch: you pay 102% of the full premium — your share plus your employer’s contribution plus a 2% administrative fee. That makes COBRA one of the pricier options.

Important note: COBRA prevents you from contributing to a Health Savings Account (HSA). If maximizing tax advantages matters to you, compare COBRA carefully against ACA Marketplace plans before enrolling.

Best strategy: Get your COBRA details from your former employer but don’t enroll immediately. Shop the ACA Marketplace first. For most freelancers, marketplace plans with subsidies win on cost. COBRA makes more sense if you’re in the middle of active treatment or have already met your deductible for the year.

5. Health Savings Accounts (HSAs) — Maximize Your Tax Benefits

An HSA isn’t a health plan on its own, but pairing one with a High-Deductible Health Plan (HDHP) is one of the smartest financial moves a freelancer can make. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free — a rare triple tax advantage.

For 2025, HSA contribution limits are:

- Individual: $4,300

- Family: $8,550

Unlike Flexible Spending Accounts (FSAs), HSA funds roll over indefinitely. You can accumulate years of savings to cover future medical expenses or even use the account as a supplemental retirement fund.

Starting in 2026, all Bronze and Catastrophic ACA plans are automatically classified as HDHPs, making HSA pairing more accessible than ever for freelancers.

6. Freelancers Union and Association Plans

Professional associations and freelancer organizations often negotiate group health insurance rates that individual freelancers can’t access on their own. The Freelancers Union is one well-known example, offering plans tailored to independent workers in select states.

Other associations worth exploring include:

- Industry-specific professional groups (writers’ associations, tech guilds, design communities)

- Local chambers of commerce

- The National Association for the Self-Employed (NASE)

These plans can be especially competitive in states where ACA provider networks are limited or where PPO options are scarce.

7. Short-Term Health Insurance

Short-term plans offer lower premiums and quick enrollment, making them useful as a temporary gap solution — for instance, while waiting for an ACA open enrollment period or transitioning between projects.

However, use these cautiously. Short-term plans are not ACA-compliant, which means they can:

- Exclude pre-existing conditions

- Cap total coverage amounts

- Exclude maternity care or mental health services

They’re a bridge, not a long-term solution.

Smart Strategies to Lower Your Health Insurance Costs

Knowing your options is only half the battle. These practical strategies help freelancers cut costs further:

- Estimate your income accurately. Since ACA subsidies are based on projected annual income, reporting your best estimate helps you get the right subsidy upfront and avoids repayment surprises at tax time. Update your Marketplace account if your income changes significantly mid-year.

- Deduct your premiums. Self-employed individuals can deduct 100% of health insurance premiums from their federal taxable income. This is a significant tax break that reduces your effective cost of coverage.

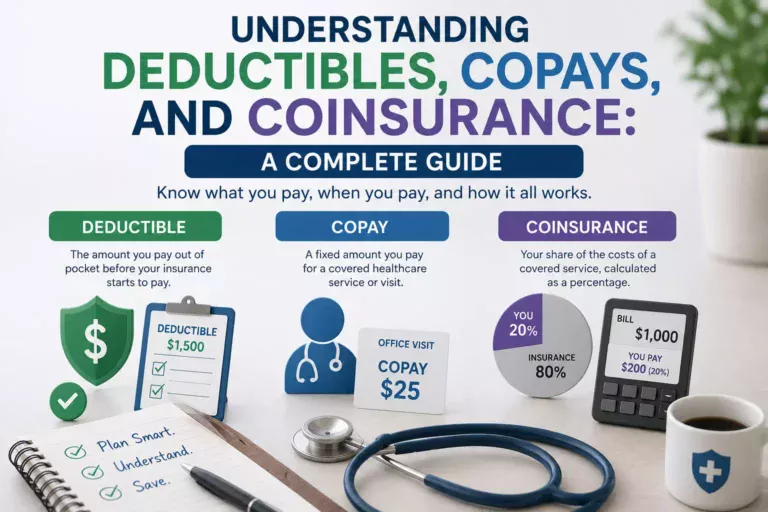

- Compare total costs, not just premiums. Factor in deductibles, copays, and out-of-pocket maximums. A plan with a lower monthly premium but a $7,000 deductible may cost more overall if you use healthcare regularly.

- Consider telehealth memberships. Services like Teladoc or MDLIVE offer virtual consultations for a monthly fee, reducing the need for costly in-person visits and complementing high-deductible plans effectively.

- Shop every year. Rates and plans change annually. A plan that was the best value last year might not be this year. Review your options during every open enrollment period.

Choosing the Right Plan: A Quick Decision Guide

Not sure where to start? Answer these questions to narrow your options:

- Is your income below 138% of the federal poverty level? → Check Medicaid eligibility first.

- Does your spouse have employer coverage? → Compare their plan’s cost of adding you vs. individual marketplace plans.

- Did you recently leave a job? → Get COBRA details but compare to ACA plans before enrolling.

- Are you young and generally healthy? → A Bronze or Catastrophic plan paired with an HSA may be your best value.

- Do you use healthcare regularly? → Silver or Gold plans reduce your costs when you actually need care.

- Do you belong to a professional association? → Check if group health plans are available through your membership.

Frequently Asked Questions

Can freelancers get health insurance subsidies?

Yes. Most freelancers qualify for ACA premium tax credits if their income falls between 100% and 400% of the federal poverty level. Many qualify for even deeper savings through Cost-Sharing Reductions on Silver plans.

What is the best health insurance for self-employed workers?

For most freelancers, an ACA Marketplace Silver plan offers the best balance of premium, deductible, and out-of-pocket costs — especially with subsidies. Higher earners may benefit from working with a licensed broker to explore off-exchange options.

Can freelancers deduct health insurance premiums?

Yes. Self-employed individuals can deduct 100% of health insurance premiums paid for themselves and their families directly from their federal taxable income, reducing their overall tax burden significantly.

What happens to my health insurance if my income changes?

You should update your income estimate on the ACA Marketplace as soon as possible. Your subsidy will adjust accordingly. Significant income drops may also make you newly eligible for Medicaid.

Is COBRA worth it for freelancers?

Rarely, unless you’re currently in treatment or have already met your deductible. COBRA is typically expensive, and most freelancers find ACA Marketplace plans with subsidies to be far more affordable. Always compare both before deciding.

What is an HSA and how does it help freelancers?

A Health Savings Account (HSA) lets you set aside pre-tax money for medical expenses. Paired with a qualifying high-deductible plan, it offers a triple tax advantage — deductible contributions, tax-free growth, and tax-free withdrawals for qualified healthcare costs.

Conclusion

It takes some investigation to get reasonably priced health insurance for independent contractors, but it is completely doable. The most significant action that most independent contractors may do is to check their eligibility for subsidies via the ACA Marketplace at healthcare.gov. Next, evaluate the Medicaid alternatives offered by your state, find out if a spouse’s plan is available, and think about combining a high-deductible plan with an HSA to save money over time.

Avoid being uninsured due of the complexity. The appropriate plan safeguards both your livelihood and your health. Every enrolment period, take the time to evaluate your options, account for tax credits and deductions, and select coverage that meets your healthcare requirements as well as your actual income as an independent contractor.