You followed the procedure, saw a doctor, and have health insurance, therefore you did everything correctly. Then a bill arrives that’s twice what you expected. Does that sound familiar? You’re not by yourself. One in three insured adults have received a medical bill that was higher than anticipated, according to a KFF Health Tracking Poll. One of the most annoying aspects of using the American healthcare system is dealing with unexpected medical expenditures, many of which are avoidable.

This book explains what exactly results in unexpected medical bills, your legal rights as a patient, and the doable actions you can take to safeguard your finances before to, during, and following a hospital visit.

What Is a Surprise Medical Bill?

A surprise medical bill, often known as a “balance bill,” is an unforeseen expense that usually occurs when you obtain care from an out-of-network physician, frequently without your knowledge. It is described by the Consumer Financial Protection Bureau (CFPB) as an unforeseen bill for services that you were unaware were out-of-network until after the fact.

- Surprise bills frequently arise in the following circumstances:

- ER visits by an out-of-network ER doctor at an in-network institution

- scheduled procedures where the radiologist or anaesthesiologist is not in the network

- Your in-network physician may request lab work or imaging, but it may be routed to an out-of-network facility.

- Transporting ambulances by air in an emergency

It can be really expensive. Of the 1 in 5 Americans who received an unexpected medical bill in a recent year, 22% were charged over

Know Your Rights: The No Surprises Act

Since January 1, 2022, the No Surprises Act (NSA) has provided federal protections against many forms of balance billing. Here’s what it does for you:

| Situation | Your Protection |

|---|---|

| Emergency care from out-of-network provider | You pay no more than your in-network cost-sharing amount |

| Out-of-network provider at an in-network facility | Protected from balance billing |

| Air ambulance (in most cases) | Capped at in-network cost-sharing |

| Uninsured / self-pay patients | Providers must give a Good Faith Estimate |

Before your scheduled service, providers are legally obligated to provide you with a written Good Faith Estimate (GFE) if you are uninsured or decide not to use your insurance. You have the right to contest your final bill through a federal resolution process if it exceeds the GFE by $400 or more. However, you must do it within 120 days of receiving the bill.

Pro Tip: Always save a copy of your Good Faith Estimate. It’s your legal record if a billing dispute arises.

8 Practical Ways to Avoid Unexpected Medical Bills

1. Verify That Every Provider Is In-Network — Not Just the Facility

The most prevalent trap is this one. The surgeon, anaesthesiologist, assistant surgeon, or radiologist working at your hospital could not be in-network, even though you have verified that your institution is. Request a complete list of all the providers who might be involved in your care from the billing department prior to any scheduled procedure. Then, call your insurer to confirm each provider’s network status.

2. Ask for a Good Faith Estimate Before Any Scheduled Procedure

Even if you have insurance, you can request a written cost estimate before treatment. Confirm the CPT code (Current Procedural Terminology) for your procedure — these are the billing codes insurers actually use to process claims. Once you have the code, run it by your insurer to confirm coverage. Medical billing staff can easily provide CPT codes upon request.

3. Understand Your Plan Before You Need It

Don’t wait until you’re sick to read your benefits. Key terms every patient should know:

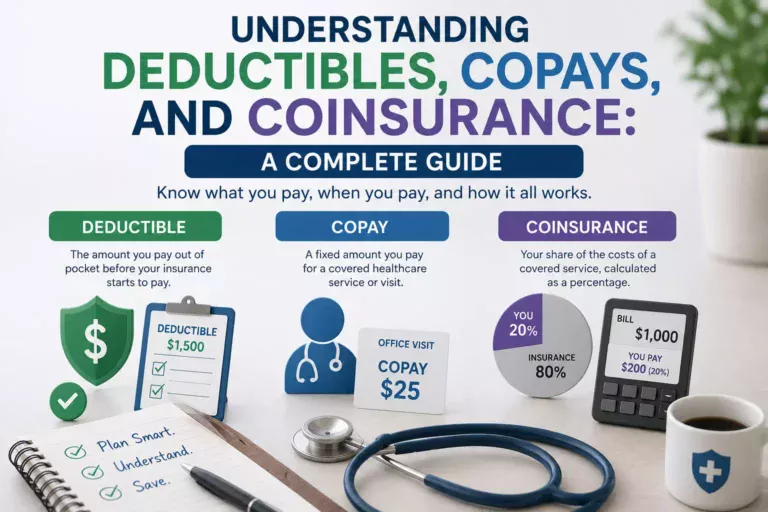

- Deductible — What you pay out-of-pocket before insurance kicks in

- Copay — A fixed amount you pay per visit

- Coinsurance — Your percentage share after the deductible is met

- Out-of-pocket maximum — The most you’ll ever pay in a policy year

- Prior authorization — Approval required for certain procedures before they happen

Many people are surprised to learn that even “covered” services may cost money if the deductible hasn’t been met yet.

4. Don’t Assume Preventive Care Is Always Free

Most insurance plans cover preventive services — annual physicals, mammograms, colonoscopies — at 100% with no cost-sharing. However, if your doctor bills a separate diagnostic code during that same visit (say, for discussing a symptom), it may be billed differently and trigger a copay or deductible charge. Always ask your provider how the visit will be coded before it happens.

5. Shop Around for Non-Emergency Services

For planned procedures like MRIs, blood panels, or outpatient surgeries, costs can vary dramatically between facilities. The same MRI might cost $400 at an independent imaging center and $2,000 at a major hospital. Many insurers now offer online cost estimator tools that show expected costs by procedure and location. Use them — and don’t hesitate to ask your doctor for a cost-effective referral.

6. Request a Preauthorization (and Get It in Writing)

For any major procedure, call your insurer and ask whether prior authorization is required. If it is, work with your provider’s office to complete the paperwork before the service is rendered. Always request written confirmation of approval — verbal assurances are not enough. Without written proof, you may be unable to dispute a denied claim later.

7. Review Your Explanation of Benefits (EOB)

After receiving care, your insurer sends an Explanation of Benefits — a document showing what they paid and what you owe. Many people ignore it because it says “This is not a bill.” Don’t. Compare it carefully against the actual bill you receive. Billing errors are more common than most people realize, and catching discrepancies early can save you hundreds of dollars.

8. Build an Emergency Medical Fund

Even with strong insurance and careful planning, some costs are genuinely unpredictable. A practical rule of thumb: set aside an amount equal to your plan’s annual out-of-pocket maximum in a savings or Health Savings Account (HSA). That way, even a worst-case scenario won’t destabilize your finances. Some employers also offer Flexible Spending Accounts (FSAs) that let you pay medical costs with pre-tax dollars.

What to Do If You Already Received a Surprise Bill

If a surprise bill has already landed in your mailbox, you’re not out of options:

- Don’t ignore it. Unpaid medical bills can be sent to collections and affect your credit.

- Review the itemized bill. Request a line-by-line breakdown and look for errors, duplicate charges, or services you didn’t receive.

- Call your insurer. Ask them to re-process the claim if it was incorrectly categorized.

- Invoke the No Surprises Act. If your bill is $400 or more above your Good Faith Estimate, file a dispute at CMS.gov or call 1-800-985-3059.

- Negotiate directly. Many hospitals have financial assistance programs or will negotiate a payment plan. Ask specifically for a “prompt pay” discount if you can pay a lump sum.

- Contact a patient advocate. Organizations and professionals specialize in disputing medical bills on your behalf.

Quick Reference: Before, During & After Your Visit

| Timing | Action |

|---|---|

| Before the visit | Verify in-network status of all providers; request Good Faith Estimate; confirm prior authorization if needed |

| At the visit | Ask how the visit will be coded; confirm all services performed are covered |

| After the visit | Review EOB carefully; compare it to your itemized bill; dispute errors promptly |

Frequently Asked Questions

What is the No Surprises Act and how does it protect me?

The No Surprises Act, effective January 2022, prevents providers from balance billing you for emergency care and most out-of-network services at in-network facilities. You pay only your in-network cost-sharing amount.

Can I be balance billed if I go to an in-network hospital?

Yes, if an individual provider treating you (like an anesthesiologist) is out-of-network. However, the No Surprises Act now prohibits most of these charges without prior written consent.

What is a Good Faith Estimate?

A Good Faith Estimate is a written cost breakdown a provider must give you before scheduled care. Uninsured and self-pay patients are legally entitled to one; insured patients can also request one.

What should I do if my bill is higher than my Good Faith Estimate?

If your bill exceeds your GFE by $400 or more, you can dispute it within 120 days through the federal patient-provider dispute resolution process at CMS.gov.

Are emergency room visits covered by the No Surprises Act?

Yes. For emergency care, out-of-network providers cannot charge you more than your plan’s in-network cost-sharing amount, regardless of where you receive treatment.

What is balance billing?

Balance billing is when a provider bills you for the difference between their full charge and what your insurer paid — the “balance.” The No Surprises Act restricts this in many situations.

Do I need prior authorization for every procedure?

Not every procedure, but many surgeries, specialist referrals, imaging tests, and brand-name medications require prior approval. Always check with your insurer before scheduled care to avoid a denied claim.

Conclusion

Unexpected medical expenses don’t have to be unavoidable. You may significantly lower the chance of financial surprises following a medical visit by being aware of your insurance plan, asking for written cost estimates, confirming provider network status prior to each appointment, and being aware of your rights under the No Surprises Act.

Although the healthcare billing system is complicated, you have more power than you may realise if you ask the correct questions at the appropriate time. Be proactive, maintain documentation, and never be afraid to contest a charge that doesn’t seem correct. Your physical and financial well-being are equally crucial.